Software sector valuations have just been jolted by a jolt: over $400 billion has evaporated in just a few trading sessions. Investors are suddenly taking seriously the idea that AI could replace some traditional software and business models.

The Flash Crash That Shook the Software Industry

In just a few days, an entire segment of the tech industry has gone into correction mode:

- Over $400 billion in market capitalization has evaporated in software stocks following the announcement of a new wave of “agentic” AI tools capable of coding and executing tasks end-to-end.

- The Wall Street Journal estimates that approximately $300 billion has been wiped out across two S&P indices that include software publishers, financial data companies, and market platforms.

- In the same move, Microsoft alone lost nearly $380 billion in market capitalization in just one or two trading sessions following its earnings release, despite very strong growth in cloud computing and AI.

One strategist sums up the market psychology: “Valuations were already reflecting near-perfect execution. The slightest doubt about the ability to monetize AI triggered a sharp revaluation.”

Where does the fear come from? AI that “eats” software

AI tools that are starting to replace entire building blocks. The immediate trigger for this sell-off was Anthropic’s presentation of a new generation of tools:

- A code generation tool presented as capable of producing complete applications on demand;

- AI agent “coworkers” and plugins designed to function like digital colleagues, capable of orchestrating existing software workflows.

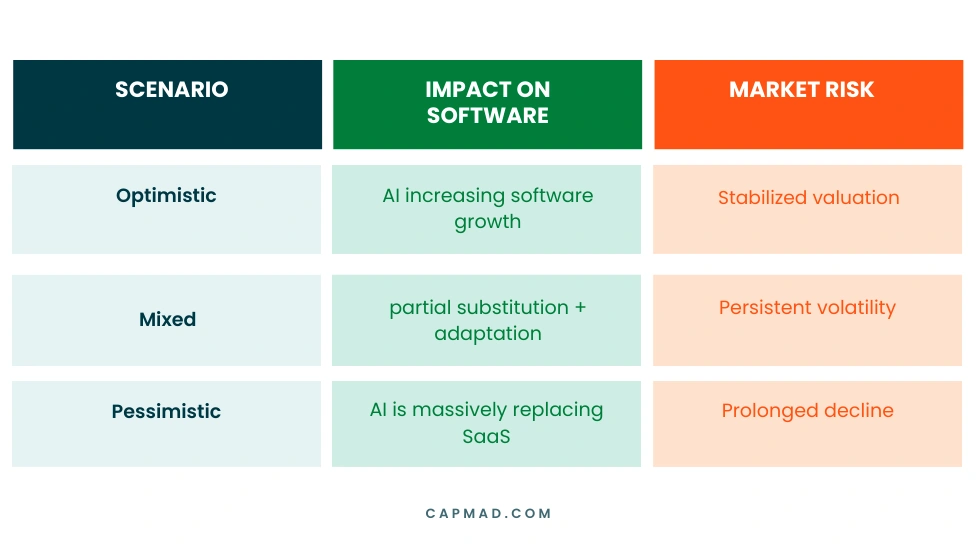

Evolution Scenario

The SaaS Logic Challenged

In an analysis that went viral, a market observer describes the situation as the “Great Software Correction of 2026”:

- In the classic SaaS model, growth relied on selling licenses per user. The more employees, the more “seats” the company paid for.

- By automating workflows, AI reduces the need for human seats. Companies can “insource” functionalities via AI agents and scripts, rather than multiplying subscriptions to specialized tools.

- The result: instead of buying ten licenses for a CRM or HR tool, a company can ask an AI agent to interact directly with its databases and APIs to generate interfaces and reports on the fly.

Conceptual illustration to be integrated

As a macro-strategist quoted in this analysis writes: “The need for software sold in seats is evaporating, because AI allows companies to no longer pay for the process, but for the result.”

Quotes and Perspectives: What the Players Are Saying

Several striking phrases are circulating in market commentary and interviews:

Shelby McFaddin, manager of a $2.6 billion fund, explains:

AI isn’t just going to affect work… it’s going to impact profits too.

A strategist compares the situation to a textbook case of disruption:

This is BlackBerry time for software: the industry will survive, but the old model will never truly return.

In an essay on the “AI Enterprise Index,” an analyst states:

If companies don’t adopt AI, they will be overtaken by it.

On a psychological level, Sam Altman confessed to feeling “useless” using his own model for coding, and that engineers are witnessing a “death of the community” as AI automates tasks that were once collaborative.

These quotes support the idea of a shift: AI is no longer just a productivity tool, but an existential threat for some software publishers.

The fundamentals: solid results, but an unforgiving market

The paradox is that this decline comes at a time when the fundamentals of several giants remain robust. Microsoft is a prime example:

- Cloud revenue of $51.5 billion, up 26%,

- Intelligent Cloud segment up 29%,

- Azure + other cloud services: +39%, driven by AI workloads, with 15 million paid seats for Copilot in Microsoft 365,

- Remaining performance obligation of $625 billion, up more than 100% year-over-year, 45% of which is related to commitments around OpenAI.

Yet, the stock market value has plummeted:

- The main reason, according to several analysts, is the explosion of AI capital expenditures: the market fears that the $500 billion in cumulative investment spending planned for 2026 by Microsoft, Meta, Alphabet, and Amazon will not produce the expected returns.

- Massive spending on AI is only acceptable if future growth more than compensates – at the slightest doubt, the penalty is immediate.

Key trend: The “great rotation” in software stocks

Several sources (Axios, CNBC, WSJ) point to the following trend:

- Software sector indices have entered a bear market, with declines of approximately 25% from recent highs;

- flows are shifting towards “AI winners” on the end-user side (industry, biotech, energy), which are improving their margins through AI rather than selling it as a product.

Two stories are emerging graphically:

- a downward curve in the valuation multiples of generalist SaaS providers,

- an upward curve in productivity and profitability in “old economy” sectors that are integrating AI to optimize their operations.

Beyond the Market Hype: Is AI Really Replacing Software?

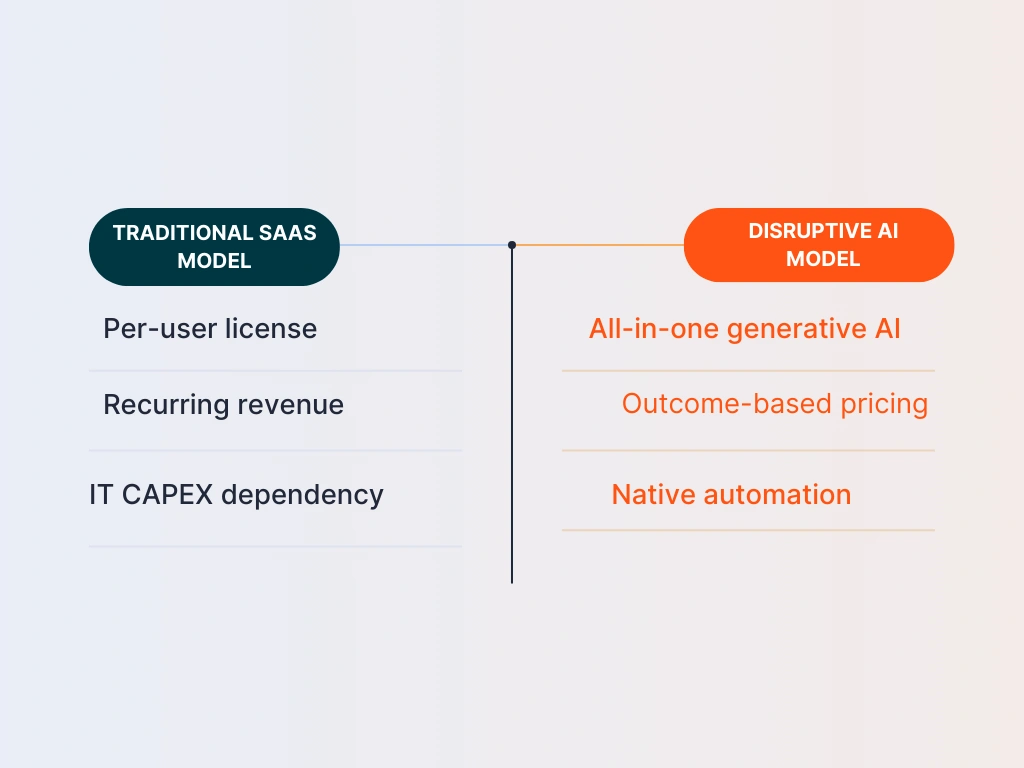

The phrase “AI eats software” is deliberately provocative, but the reality is more nuanced:

- Many experts point out that AI is grafted onto existing software: ERPs, CRMs, HR tools, and financial systems remain the backbone, and AI functions as an orchestration layer.

- Some software vendors are already adapting by pivoting to “AI-native” offerings: software designed from the ground up to be operated by agents, billed based on results (transactions, automated tasks) rather than at headquarters.

- According to Gartner, cited in several analyses, 33% of enterprise applications could integrate “agentic AI” within a few years, compared to less than 1% today.

In other words, it is not so much “the software” that disappears, but rather certain monetization models (perpetual licenses, head office billing, redundant suites) that become difficult to justify.

Sector-specific illustration: who risks what?

We can outline three groups of players:

The most exposed:

- redundant office suites and horizontal tools,

- general-purpose no-code/low-code software facing competition from app generation agents,

- software vendors adding AI as a simple “marketing feature” without revising their business model.

The adaptive ones:

- integrated cloud platforms that sell both infrastructure and AI services,

- vertical vendors (healthcare, industry, energy) that inject AI into highly specific and difficult-to-replicate stacks.

The indirect winners:

- capital-intensive industries (heavy industry, biotech, logistics) that use AI to optimize their costs,

- companies capable of leveraging new tools without being software vendors themselves.

A Forbes analyst summarizes: “While fear of AI weighs on software stocks, many industrial and biotech companies are seeing their margins soar thanks to AI.”

Macroeconomic stakes: capital expenditure, energy, misallocated capital?

The debate goes beyond just tech:

- The AI race could become “one of the biggest cycles of capital misallocation in history” if monetization doesn’t keep pace with capital expenditure, warns a widely discussed analysis.

- Data centers have colossal energy needs, potentially straining the grid, and necessitating a trade-off between AI, the energy transition, and other social investments.

Some economists are beginning to compare this phase to the telecom bubble of the early 2000s: an explosion of infrastructure investment, followed by a long consolidation where only the most robust models survive.

What can software publishers and investors do?

For software publishers, the possible solutions are converging:

- Rethink pricing: shift from “price per user” to “price per value created” (automated processes, transactions, performance);

- Become AI-first: integrate agents and decision-making capabilities into the core of the product, rather than simply adding a chatbot;

- Move up the stack: focus on areas where business knowledge, compliance, and deep integration with customer systems remain a sustainable advantage.

For investors, the current correction looks more like a structural re-rating than a simple anomaly:

- Revisit software portfolios, distinguishing between disruptive models and AI-compatible models;

- Closely monitor operational indicators: customer retention, actual adoption of AI modules, and margin evolution after accounting for compute costs;

- diversify towards sectors that capture the value of AI on the end-user side (industry, energy, health) and not just on the tool provider side.

The Psychological Factor in Tech Markets

This sudden correction reveals a deeper phenomenon: the markets’ extreme sensitivity to highly valued tech giants. In a context of very high expectations, the slightest shift in financial rhetoric can trigger excessive reactions.

Microsoft perfectly illustrates this status of a stock that has become almost “systemic.” At this market capitalization level, the company is no longer valued solely on its immediate results, but on its ability to shape the future of digital technology in the long term. Consequently, any perception of a weakening of this promise translates into brutal stock market adjustments.

Ultimately, the more than $400 billion drop in software is not just an episode of volatility: it is a live stress test of a scenario that the market had previously underestimated, one in which AI not only enhances software, but reshapes its economic landscape and the champions of tomorrow.