The figures speak for themselves. In 2024, 23 African countries were in financial distress, and three of them defaulted or requested formal debt restructuring. In total, African countries have a debt of more than $1.8 trillion. A mountain whose interest payments alone are enough to paralyze entire sectors of public finances.

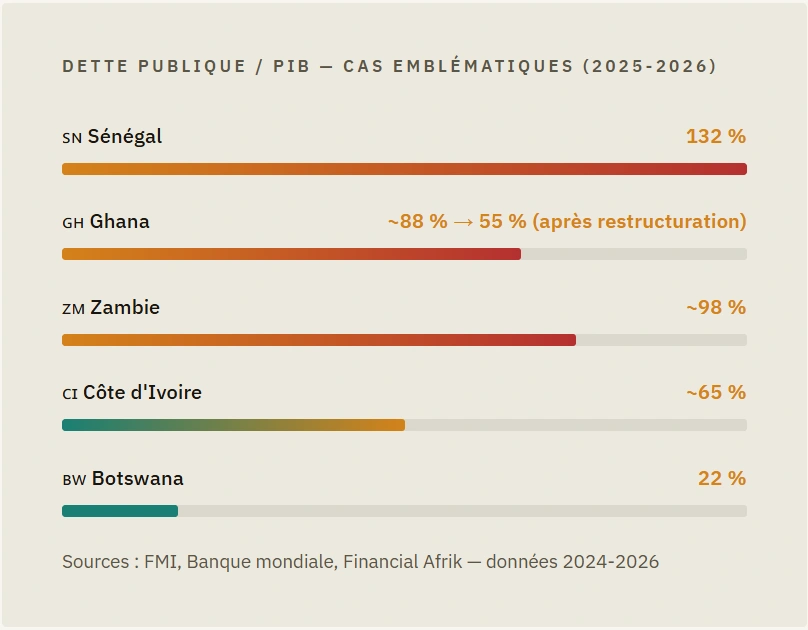

Yet, the image of a uniformly collapsed Africa is false. Public debt in the region stabilized in 2023 at around 60% of gross domestic product, a high level, but the situation remains highly varied from one country to another. Between Botswana, with its 22% of GDP, and some countries easily exceeding 100%, the African continent presents a mosaic of very different situations.

Anatomy of a Structural Crisis

To understand the African debt crisis, we must go back to its origins. After experiencing a significant decline during the 2000s, thanks to economic growth fueled by rising commodity prices and increased foreign investment, as well as debt relief, public debt in sub-Saharan Africa began to rise again in 2013.

What followed was a series of successive shocks: the fall in commodity prices in 2014-2016, the Covid-19 pandemic in 2020-2021, the sharp rise in global interest rates from 2022 onwards, and finally, the trade tensions of 2025. Each episode left budgetary scars that governments have filled… with more debt.

Excessive debt can lead to higher interest rates, stifle private investment, and cause inflation. The vicious cycle continues: the more indebted a state is, the more expensive its loans become, the less it can invest, the less it grows, and the harder it is to repay. It is precisely this cycle that several African countries are struggling to break today.

Senegal particularly exemplifies the dangers of poorly managed debt. The total debt of Senegal’s public and semi-public sectors reached 132% of gross domestic product at the end of 2024, of which approximately 4% was in domestic arrears awaiting audit. The authorities have revealed a significant hidden debt, resulting from unrecorded liabilities under the previous administration, which has caused the debt-to-GDP ratio to balloon to 132%.

The consequences are immediate and painful. By 2025, interest payments represent nearly 16% of tax revenue, or one franc in six collected by the public treasury. This situation is all the more worrying given that nominal GDP growth remains below the average cost of debt, meaning that debt is growing faster than wealth is being produced.

Regional investors have been snapping up Senegalese Treasury bonds since the beginning of 2026 despite the country’s abysmal public debt. This mobilization could allow Dakar to avoid default while awaiting an agreement with the IMF. A welcome boost, but one that does not absolve Dakar of difficult structural decisions.

Ghana and Zambia: Lessons from Restructuring

Faced with the abyss, some countries have managed to recover. Ghana and Zambia are now two textbook cases with very contrasting results, guiding the continent’s strategies.

Ghana: A Benchmark Model

Ghana’s debt-to-GDP ratio fell from 88% to 55% between the start of restructuring and mid-2025. Ghana successfully completed its fifth IMF review in December 2025, unlocking an additional $385 million and confirming the gradual return of international confidence.

A 37% haircut on Eurobonds, but a coordinated process with the IMF that preserved future market access.

Zambia: Late Restructuring

Zambia’s restructuring process lasted more than three years, damaging its economy. Zambia illustrates the dangers of late restructuring: each additional month of negotiation is costly in terms of growth and credibility.

Zambia officially applied for a new IMF program in February 2026, aiming for an agreement by May.

The Gordian Knot: Private Creditors and China

One of the reasons the African debt crisis is so difficult to resolve lies in the nature of its creditors. The G20 Common Framework primarily concerns official bilateral creditors and does not require the participation of private creditors. Their participation is voluntary and non-binding. Overall debt restructuring is therefore difficult, particularly in Africa, where 43% of external debt is held by private creditors.

China, which has become the continent’s largest bilateral creditor over the past two decades, is a key player in the problem—and potentially in the solution. China demonstrated its ability to work within this framework during the Zambian debt restructuring, accepting the principle of “comparability of treatment.” This precedent paves the way for more constructive negotiations in the future.

Five solutions to break the cycle

Reform of rating systems

Credit rating methods must evolve to reflect the structural progress and reform potential of African economies, and not simply penalize volatility that African countries did not create. A pan-African rating agency is now under consideration.

Broadening the tax base

Most African countries collect less than 20% of GDP in tax revenue, compared to the global median of 27%. Broadening the tax base, digitizing tax administration, and combating tax evasion are more sustainable levers than borrowing.

Investing in local processing

Processing raw materials on the continent—minerals, cocoa, coffee, cotton—multiplies added value by 5 to 10, generates skilled jobs, and provides sustainable tax revenue. It is the most effective antidote to imported debt.

Innovative Refinancing Mechanisms

Debt-to-climate swaps, green bonds, and partial guarantee instruments from the African Development Bank (AfDB) or the World Bank allow for refinancing at lower rates while directing funds toward productive investments.

Preventive and Transparent Restructuring

The Ghanaian example proves that it is better to restructure early, transparently, and in coordination with the IMF than to wait for a disorderly default. Defining a realistic medium-term fiscal course is the first measure recommended by the IMF.

Mobilizing Regional Financial Markets

The mobilization of regional investors for Senegalese Treasury bonds in 2026 demonstrates that African financial markets can play a stabilizing role. Developing these markets further is a strategic priority for the entire WAEMU zone.