Senegal is facing a debt crisis with over €330 million due on its Eurobonds in March 2026. This makes the risk of default real, but not inevitable, if President Bassirou Diomaye Faye quickly combines fiscal adjustment, alternative financing, and a clearer strategy with the IMF and the markets.

With debt representing 132% of GDP and Eurobonds maturing next month, Senegal’s economic outlook now constitutes “the next major test for the international financial system.” Can President Faye avoid default?

A Debt Wall in March 2026

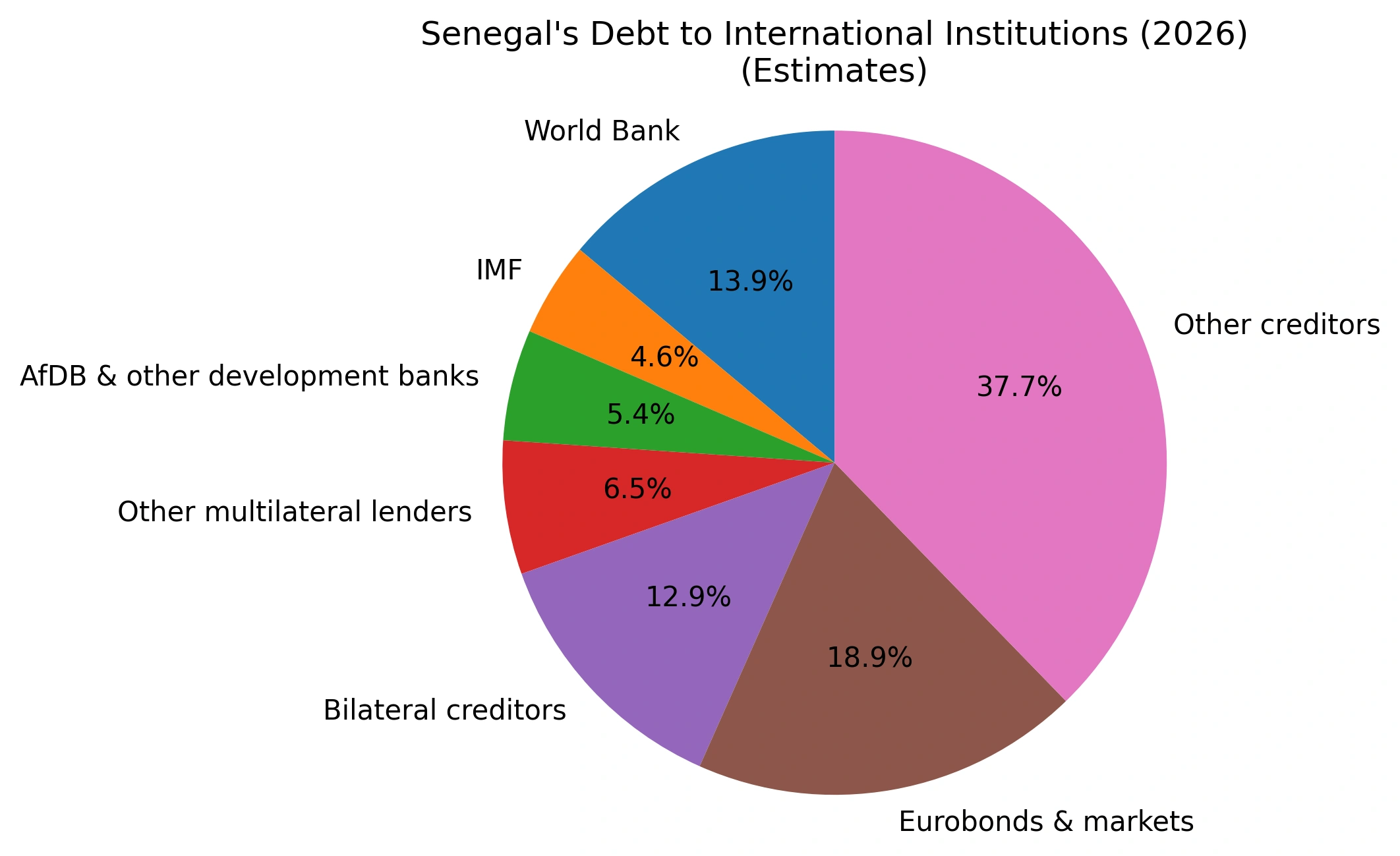

The most critical deadline will be March 13, 2026, with a repayment of approximately €333.3 million (nearly 219 billion CFA francs) on Eurobonds issued in 2018. This deadline is part of a much larger schedule, as Senegal must honor a total of approximately USD 1.1 billion in Eurobond repayments between 2026 and 2028, with nearly a third due in 2026.

Markets have already priced in this stress: several Senegalese Eurobonds are trading between 50 and 70 cents per euro face value, a level typical of situations where default or restructuring seems likely.

A Mixed Macroeconomic Situation

In real terms, the Senegalese economy remains dynamic, driven by the start of hydrocarbon and services production: the IMF has anticipated growth of around 8% in 2025, making the country one of the best performing on the continent. At the same time, inflation has been generally kept under control (around 1% in 2024, with a slight rebound expected in 2025), which limits the social risk associated with rising prices, even though pressure on public finances remains high.

On the other hand, total debt (public and semi-public) exceeds 130% of GDP according to some recent estimates, placing Senegal in the category of countries at high risk of debt distress.

Faye faces an explosive legacy

President Bassirou Diomaye Faye and his government must manage a legacy marked by a rapid accumulation of debt and a double-digit budget deficit in 2024 (around 13% of GDP). Starting in 2025, the authorities attempted an austerity program, aiming to reduce the deficit to around 7-8% of GDP, with the objective of lowering it to around 5% in 2026 and 3% in 2027, in accordance with WAEMU criteria.

This strategy requires difficult trade-offs between debt servicing, preserving social spending, and financing the political program championed by Faye and Ousmane Sonko.

Eurobonds already in stress territory

Senegalese Eurobonds lost approximately 20% of their value in three months at the end of 2025, with some trading at nearly 51 cents, representing a discount of almost 50%. This decline accelerated after the failure of an agreement with IMF disbursements in early November 2025, as well as the Prime Minister’s statement explicitly rejecting the idea of a coordinated restructuring.

For investors, these signals reinforced the scenario of a disorderly default or a political arbitration that would place debt servicing behind other national priorities.

A constrained fiscal trajectory

The Senegalese authorities have adopted an Economic and Social Recovery Program (PRES) linked to the 2026 budget. This program aims to mobilize more than 760 billion CFA francs to stabilize public finances. The government plans to continue borrowing on the markets, particularly regional markets, with more than 4.3 trillion CFA francs to be raised to refinance existing debt and cover the deficit.

This strategy implicitly relies on Senegal’s ability to continue attracting capital despite the deterioration of its risk perception and the absence, at this stage, of an IMF safety net.

Faye’s Room for Maneuver

To try to avoid a default in March 2026, the government has already begun actively managing the debt, notably through reprofiling operations on the local banking market, which reportedly allowed for the processing of over 500 billion FCFA worth of securities in 2025.

In parallel, the authorities plan to raise up to 810 billion FCFA on the domestic market in March 2026 to cope with the peak in repayments, an objective deemed “highly unrealistic” by some analysts given the tensions in the WAEMU market. These factors show that the current strategy remains fragile and dependent on the confidence of local and regional investors.

Default Avoidance Scenario: Key Conditions

For Faye to avoid a default on Eurobonds in March 2026, several conditions must be met simultaneously.

Sustained Robust Growth

Maintaining high growth (around 7-8% in 2025 and 5% in 2026) thanks to hydrocarbons and services strengthens the tax base and mechanically improves debt ratios. In the short term, however, growth does not generate enough liquidity to absorb the March debt repayment shock on its own.

A Credible Fiscal Adjustment

The rapid reduction of the deficit (from over 13% to 5-6% of GDP) must translate into concrete measures: streamlining current spending, improving tax collection, and prioritizing high-impact investments. The more credible the trajectory appears, the more willing markets are to refinance the country at less prohibitive rates.

A Clear Framework with the IMF

The lack of a disbursement agreement with the IMF played a key role in the fall of Senegalese bonds. Even a limited program, but one accompanied by targeted disbursements and accepted reforms, could improve risk perception and facilitate access to concessional financing.

Proactive liability management

An “organized” restructuring – debt swaps, extended maturities, and coordinated management with creditors – could prevent a sudden default while preserving market access. However, this scenario requires a shift in policy from the hard line adopted so far regarding restructuring and recourse to the IMF.

Tensions Between Social Promises and Discipline

Faye’s political project is based on social justice, economic sovereignty, and lowering the cost of living, which has led him to reduce the prices of certain basic goods, generating savings of over 340 billion CFA francs for households by 2025.

At the same time, the president announced a significant increase in public investment in 2026 – over 561 billion CFA francs – in education, health, infrastructure, energy, digital technology, and housing. Reconciling these social and investment ambitions with the need for fiscal consolidation is one of the key issues contributing to the risk of default.

A High but Not Fatalistic Risk of Default

Major institutions like the World Bank point out that 2026 represents a peak in Eurobond repayments in sub-Saharan Africa, with a significant refinancing risk for countries like Senegal. If international financial conditions remain strained or worsen, market access could close rapidly, making default or restructuring difficult to avoid without multilateral support.

Conversely, a combination of robust growth, a programmatic agreement with the IMF, and active debt management would offer Faye a window to avoid default in March 2026, at the cost of significant political and social concessions.